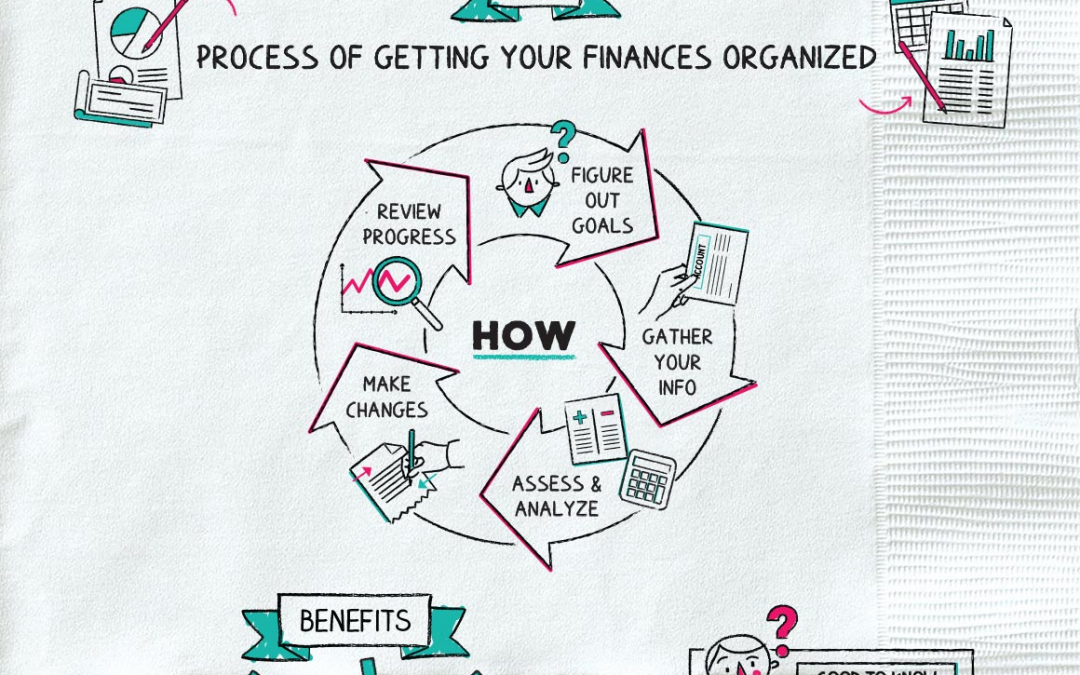

The cost of care is increasingly impacting those of all walks of life. Unfortunately, most people learn too late that Medicare DOES NOT cover Long-Term Care (LTC) insurance. And to further complicate the issue, once you need help, you are no longer able to apply for insurance. The reality is pursuing insurance protection when you are healthy, not sick.

“Washington State’s Long Term Care Trust Act is a first-of-its-kind publicly-funded program to reimburse eligible long-term services and supports (LTSS). The program will be funded by a payroll tax collected by employers on behalf of every adult W-2 employee. The rate will begin at 0.58% (fifty-eight hundredths of one percent) on “all wages” and not capped. The rate of 0.58% may be upwardly adjusted beginning January 1, 2024.”

Therefore, the State of Washington is acting in self-defense due to the exorbitant cost of care impacting their bottom line. The state needs another funding source because Medicaid has its funding limitations. Watch for pending changes in other states; Illinois is considering enacting a similar law.

What is Long-Term Care Insurance?

“Pays for help with Self-Care later in Life.”[1]

In-Home Care:

- Dressing

- Eating

- Bathing

- Continence

- Transferring

- Toileting

- Cognitive

What are your funding choices?

- Self-Funding/Self-Pay

- LTC Insurance (Traditional, Life Insurance with LTC benefits & Asset-Based Life/LTC)

- Family Pays

- Medicaid (after Asset spend-down)

As a Certified Long-Term Care specialist, I advocate for people to ensure and protect their hard-earned savings from the risk of expense cost of care with one of the many Long-Term Care insurance solutions available in the marketplace. By securing a private LTC policy, one ensures more significant potential benefits than the proposed Washington capped benefit of $36,500. An individual policy can benefit from a 6 and 7 figure benefit ($000,000 to $0,000,000) based on the personalized LTC plan.

Do you want a $ 36,500-lifetime benefit or a policy of your choosing?

Now, employees can “Opt-out” provided that they provide evidence of a certified Long-Term Care (LTC) Insurance policy by November 1, 2021. A good option for the younger generation is a Life Insurance Hybrid policy that includes LTC benefits, creating two real benefits for their beneficiaries and another funding source should they need “Hands-On” Assistances in the future.

Act TODAY! Share this critical information with anyone you know whose employed with a Washington-based company. If they are interested in pursuing, they MUST act ASAP because the proof of coverage deadline is November 1, 2021. The application underwriting process can take up to 2 months or more.

Get your Free quote TODAY!

Eleonore Weber, CLTC

Your Life Security, LLC

https://yourlifesecurity.com

© Your Life Security, LLC 2021. All Right Reserved.